More Troubling Retirement Statistics… What To Do About It… 38 Securities Yielding Over 5%

I run across a lot of statistics in my job. It comes with the territory. But I saw one a couple of years ago that truly shocked me.

Here it goes… Earlier this year, Bankrate reported that just 44% of Americans surveyed said they could afford to comfortably cover an unexpected $1,000 expense (like a car repair or hospital bill) from their savings.

I could cite dozens of studies and surveys that report similar findings. And they all come to a similar, sobering, conclusion to say the least. Millions of workers haven’t put away the first dime from their paychecks in either an IRA or 401(K). And the majority of the population only has a few hundred dollars in the bank. That’s barely enough to cover an unexpected expense like a fender bender or broken air conditioner. In fact, most respondents said they would be forced to use a credit card for such an event.

Nobody wants an unexpected bill to cause real financial hardship. That’s why most financial gurus recommend keeping an emergency fund equal to at least three months’ salary. But many workers have barely managed to save three days’ salary, let alone three months.

So how will these people fund retirement expenses when the paychecks stop coming in? Let’s just say that luxurious vacations to Tahiti are probably off the table. Maybe that’s why some people’s retirement planning consists of lottery tickets… and prayer. But fear not. Even if you’re a little behind (and statistically speaking, many are), a comfortable retirement is still in reach. It’s never too late to start building a stockpile.

More Troubling Statistics…

I broke into this business as a financial advisor. In a job like that, you witness firsthand the struggles many families face when trying to start a retirement fund. I met with people from all walks of life, from young hairdressers to powerful attorneys. And regardless of background, most are far more concerned with meeting today’s needs than worrying about a distant retirement 10 or 20 or 30 years in the future.

Besides, the cost of living is going up faster than our paychecks. Take a look at the chart below, courtesy of the St. Louis Fed. From 1999 all the way through 2016, real wages (adjusted for inflation) weren’t just stagnant — they declined! So after the car and house payments, utilities, grocery bills, and other expenses, there might not be much leftover disposable income to send to your broker.

Source: St. Louis Federal Reserve

From the late 1950s through about 1975, the average American saved between 10% and 15% of their annual income (a percentage most advisers still recommend today). But that rate began to slide in the 1980s and 1990s. For a brief period following the 2009 recession, it actually dipped to a negative 2.1%. That means for every dollar of income, we spent $1.02. Needless to say, you can’t build a nest egg that way. All you can do is dig yourself deeper into debt.

Of course then the Covid-19 pandemic struck. Forced to stay at home, and with record amounts of stimulus money flowing to Americans, the savings rate skyrocketed for a time. But as you can see from the chart below, the pandemic was something of an anomaly.

Source: St. Louis Federal Reserve

Now, the savings rate has since fallen back to about 5%. Covid may have fundamentally changed our habits for some things, but as far as saving money goes, it seems like we’re right back to our old ways.

In theory, workers approaching retirement age should be much closer to their goals, considering they’ve had decades to save and invest. But as SmartAsset points out, the median retirement 401k/IRA balance for ages 55-64 is $89,716. That’s certainly better than the $65,000 among all adults, according to the Fed’s most recent data (2019). But it’s not even in shouting distance of what most of us will need.

What about Social Security? Well, as I explained in this article, I personally don’t count on seeing a penny of all the money that has been confiscated from my paycheck and put into the system. If I do, great. But the demographics are just too daunting.

Any drastic overhauls are more likely to affect workers in their 30s and 40s than those who are closer to retirement age. Still, even in the best-case scenario, this popular safety net was never meant to be a primary source of retirement income — only a supplement.

What You Can Do About It

My intent isn’t to scare anyone. Instead, it’s to raise this question…

If you find yourself in a position of not being where you want to be, then what should you do?

In a future article, I’m going to give three easy steps that most investors can take to improve their retirement situation. You’ll find nothing wild or crazy in these ideas, but they’re essential if you want to get ahead (or catch up).

In the meantime, another crucial step, of course, is to have a group of stocks in your portfolio that reward you year after year. And in my experience, there’s no better way to do that than with a solid portfolio of income-paying securities.

And if you think it’s next to impossible to find high yields in this market, then I’ve got news for you. As I often tell my longtime readers, the high yields are out there, you just need to know where to find them…

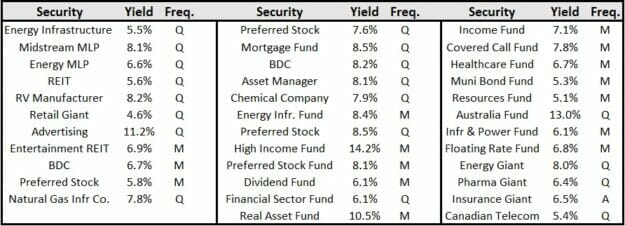

In fact, I’ll prove it to you. Over at High-Yield Investing we hold no less than 38 securities that pay more than 5% yields in our portfolio right now. Considering the average S&P 500 stock yields 1.7%, I’d say that’s pretty good…

Your average investor has never heard of the stocks, funds, and other securities we talk about in High-Yield Investing. They don’t get a lot of coverage in the mainstream financial media. That’s fine with me.

But if you’re looking for mouth-watering yields like this, then that’s where my latest report comes in…

I put this report together for readers who want to “keep it simple” — giving readers 5 safe, high-yield stocks that you can own for the long-term. I consider each one of these picks to be “bulletproof” because they have weathered every dip and crash over the last 20 years and still handed out massive gains over time. And if history is any guide, they should continue doing so for years to come.