The (Dis)Inflation Roller Coaster, A Mega Oil Deal, A 216% Gain (More On The Way?)

Folks, Nathan has done it again.

In case you missed this week’s news, ExxonMobil (NYSE: XOM) announced a mega-deal that shook the market. It will be transformative for XOM, the Permian Basin, and the entire energy sector.

If history is any guide, it could unleash a wave of deals in the energy sector – the likes of which we haven’t seen in at least three decades.

And Nathan pretty much predicted the whole thing three years ago.

Talk about being ahead of the curve. But it’s one thing to make a bold call and be right – it’s an entirely different matter to actually deliver profits.

Check on that one, too. Investors who had the gumption to follow Nathan’s recommendation tripled their money.

I’ll hand things over to Nathan in just a sec to tell you all about what went down – plus what he thinks is in store next (and how to profit).

But first, let’s talk a little bit about the latest inflation numbers.

📈 The (Dis)Inflation Roller Coaster Stalls 🎢

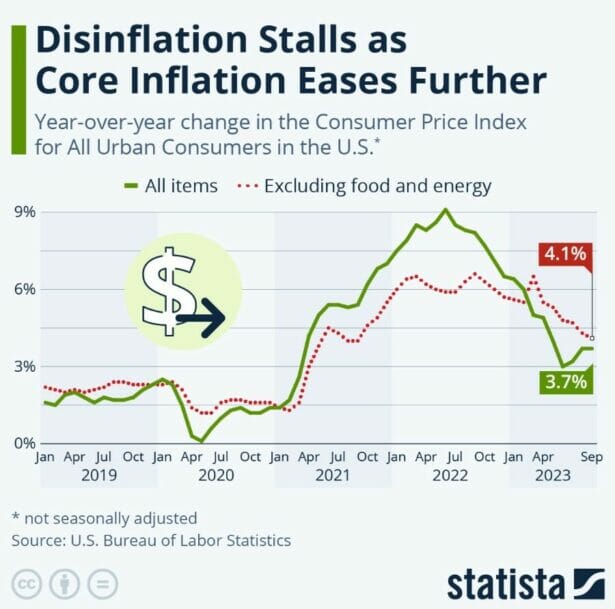

This week, the U.S. Bureau of Labor Statistics released inflation numbers for September.

The Consumer Price Index (CPI) continued its ascent, rising by 3.7% year-over-year. That matches August’s pace and slightly outpaced predictions of a 3.6% increase. On a month-to-month basis, it increased 0.4%, a bit softer than August’s 0.6%.

Source: Statista

Diving deeper, core inflation — which excludes the volatile food and energy prices — cooled down to 4.1% in September, marking its lowest since the same month last year.

Housing costs remain a significant driver of inflation. Rents and the costs associated with homeownership (owners’ equivalent rents) surged by 7.4% and 7.1% year-over-year, respectively. If we set aside these shelter costs, inflation was a more modest 2.0% in September. Exclude food, and it drops further to 1.6%.

But let’s be careful here. My intention is to point out that these two key elements of people’s lives are significant drivers of inflation. Not to imply that the inflation battle is over. Unlike New York Times columnist Paul Krugman, who said exactly the opposite.

Good news. If you don’t consume energy, don’t eat, don’t buy a house (or pay rent), and don’t need to buy a car, you’re in pretty good shape! And to think Krugman is a Nobel Prize-winning economist. But years ago, he discovered being a serious academic paid a lot less than carrying water for the bureaucratic establishment.

Anyway, it looks like there may be more work to do in the inflation fight. The job market is still robust. Consumer spending has been strong, but there are signs of fatigue (all-time high credit card balances and student loan repayments resuming). Housing prices are still sky-high.

The implications for potential rate hikes remain uncertain. While the consistent inflation trend suggests a need for intervention, the recent slowdown in month-to-month and core inflation might signal the Federal Reserve to maintain its current stance. Right now, the CME FedWatch Tool is showing a near-certainty that the Fed will hold rates steady in November, but a 30% probability for yet one more quarter-point rate hike in December.

This Mega Oil Deal Tripled Our Money. And More Big Deals Could Be Coming…

On Friday, October 6, the Wall Street Journal leaked word that Pioneer Natural Resources (NYSE: PXD) is in late-stage takeover talks with none other than Exxon Mobil (NYSE: XOM).

The rumors had been circulating for a while. But this courtship really started in April when the two companies reportedly met for preliminary discussions, which I discussed here. The news spread quickly through the media gossip mill, providing a nice jolt to PXD. But all has been quiet since then — until now.

So when fresh news of a possible union began circulating on October 6, propelling PXD to the top of the market leaderboard.

For those of you who may not know, I identified PXD as one of my first targets over at Takeover Trader – back in May 2020.

All I can say is that, sometimes, patience really pays off. Because this week, we learned that a deal was officially accepted. The price tag? A cool $59.5 billion.

In just a moment, I’m going to tell you why this could be just the beginning of a mega-wave of deals in the oil patch. But first, let’s take a look at this game-changing deal.

The Background

It is no surprise that Pioneer has attracted an interested suitor. Let’s quickly revisit a comment from my initial recommendation in 2020…

Pioneer is one of the largest remaining Permian Basin pure-plays (all others have already been taken out). It boasts 680,000 net acres that are brimming with 20,000+ potential drilling locations. Much of this contiguous acreage is in the sweet spot of the Midland Basin, which is shallower than the nearby Delaware Basin, meaning lower drilling costs. And it holds higher-grade crude that typically commands a premium price.

Side note: this was during the pandemic when oil prices bottomed near $35 per barrel. But even at that level, Pioneer’s highly efficient, low-cost wells were expected to generate $2.3 billion in operating cash flows that year, enough to cover its spending needs with $800 million in free cash flow (FCF) to spare. Here’s more from my original profile…

Pioneer’s best-in-class assets produce the highest returns per barrel in its peer group – which means fat margins even in downcycles. If it can gush cash at $35 per barrel, imagine what it can do if prices recover to $50.

Well, that’s not a hypothetical question anymore. Thanks in part to OPEC+ production cuts, benchmark crude prices have rebounded to near $90 per barrel.

Even if they retreat to $60, Pioneer would deliver $13 billion in cumulative free cash flow over the next five years. At $80 per barrel, those profits would double to $27 billion.

Source: Pioneer Investor Presentation

That’s enough to move the earnings needle — even for a supermajor like Exxon Mobil.

Swallowed By A Bigger Fish

In recent years, Pioneer has been on the buying end of these deals. Most notably, it took control of Permian peers such as Parsley Energy and Double Point Energy for a combined $11 billion. But as they say, there’s always a bigger fish.

The hunter has become the prey.

After overpaying for XTO Energy more than a decade ago, Exxon Mobil has been biding its time and hoarding cash — pocketing $59 billion in net income last year alone. The company has well-known aspirations in the Permian Basin, outlining a production target of 1 million barrels per day in West Texas by 2025.

Pioneer would help it reach that goal ahead of schedule, bumping its Permian output to 1.33 million barrels of oil equivalent per day. For context, that’s more than the OPEC nation of Libya.

It’s a bit premature to delve into the financial aspects, especially since there’s not even a firm offer on the table yet. As with most tie-ups, there will likely be meaningful cost-savings synergies to exploit. Combining forces would also increase negotiating clout when dealing with oilfield equipment vendors and service providers. Management may even boost the bottom line by routing some of Pioneer’s oil through Exxon’s co-owned pipelines.

The Timing Is Right

The timing is also right. Aside from its cash stockpile, Exxon’s stock has climbed 50% since the Ukraine invasion, so fewer shares of this rich currency need to be spent to close a deal. And at $60 billion, it would be paying just 6.5 times EBITDA for Pioneer. According to the WSJ, that’s a 25% discount to its historical multiple. Exxon can extend a sizeable premium at this valuation and still generate strong returns from this transaction.

Pioneer seemed receptive to a merger, considering founder and CEO Scott Sheffield recently announced his retirement. It’s a well-earned one at that. Since I first added PXD to my portfolio over at Takeover Trader, the stock has advanced from double-digit territory to a recent close of $248. Along the way, it has dished out 16 dividend distributions totaling $42 per share – bumping the total return to 216%.

If You Missed The Boat…

The WSJ is speculating that this mega-merger could unleash a new wave of consolidation in the oil patch, perhaps even rivaling the frenzied M&A activity seen in the late 1990s (back when Exxon and Mobil were still separate entities). I couldn’t agree more.

That’s exactly why every new subscriber of Takeover Trader receives a special report called the “Mother of All Oil Booms” detailing the shopping spree underway in the prolific Permian Basin.

Regardless of the industry, transformational mergers often spur the remaining players to seek out their own dance partners. That puts my top pick, which sits on prime drilling terrain 12 times the size of Manhattan, in the proverbial sweet spot.

Coincidentally, we’ve already doubled our money on this pick. But considering it’s a smaller, mid-sized fish (as opposed to a big one like PXD), it could only be a matter of time before a suitor comes knocking.